Dynatrace SaaS Stock Study

We look at an interesting stock in the highly competitive, nascent, high growth, big runaway APM/Observability industry leaving us with an awesome first impression

Disclaimer: The information provided is not financial, investment, tax or other advice. Nothing contained constitutes a solicitation, recommendation, endorsement or offer to buy or sell any securities or any other financial instruments. For more information read the disclaimer.

Dynatrace Analysis

Industry Overview

APM/ Observability solutions industry builds software for making it easier for software developers and operators to build and operate software at scale, monitor its performance and identify cost savings, troubleshoot issues quickly to have virtually 0% downtime. These solutions are very sticky as they reside next to customer’s software and indispensable for everyday business leading to high switching costs too.

Business Overview

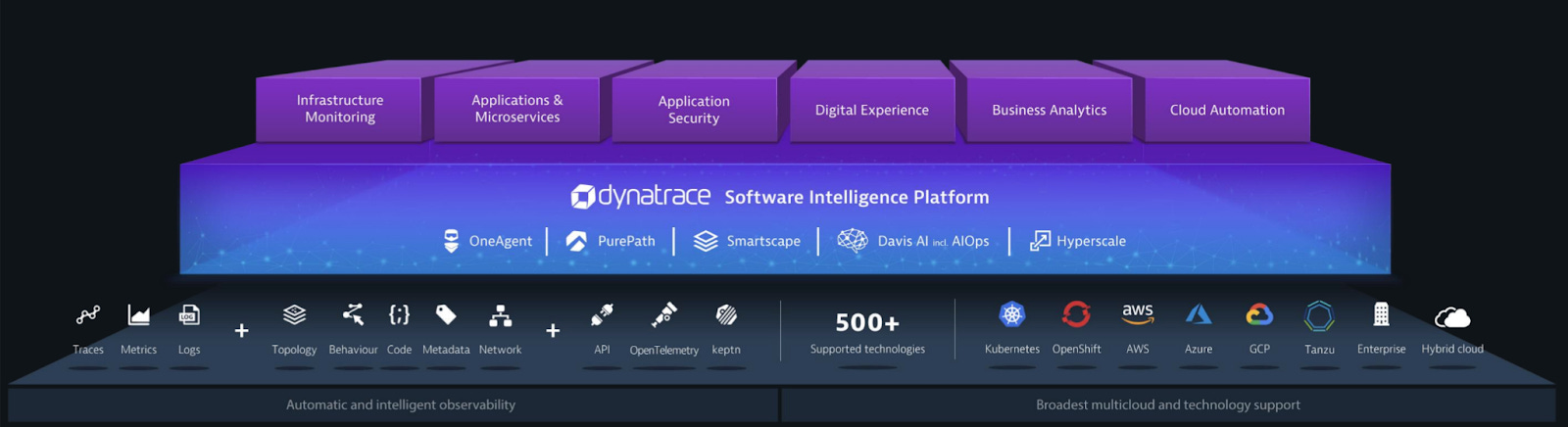

Dynatrace is a Business that primarily built its moat around building APM/Observability-based solutions for customers who run distributed computer software running in complex environments like multiple machines, muti-clouds. In recent years, they have expanded their offerings by adding software for security, automation, analytics, and AI. All these expansions are adjacent to their initial products. Their software platform is cloud-based and on-prem. This platform can be broken down into six verticals:

Infrastructure Monitoring(monitoring infrastructure like physical machines, AWS, etc)

Applications & Microservices(monitoring software applications)

Application Security(monitoring software applications for security problems during development/operating them)

Digital Experience(monitoring software user experience)

Business Analytics(general software business analytics, KPI’s)

Cloud Automation(DevOps automation)

The management tells us that the TAM for their solutions is 50B+. This tells us that there are long runaways of growth for this business. The TAM estimates are just that, estimates, take them with a grain of salt. Looking at the trajectory of Dynatrace and its competitors in terms of revenue growth, it looks like this industry is starting to pick up and the TAM might be realistic.

Their growth strategy is simple, acquire new customers and expand with current customers by cross-selling more solutions.

Dynatrace is classified as a “leader” in their core APM business by Gartner.

Competition

Primary Dynatrace competitors are Splunk, Datadog, New Relic, Elastic and Sumologic. All these companies have pretty much similar offerings. Splunk is the biggest business in this space with 2.3B ARR, I would say Splunk definitely has the biggest moat among all these businesses and Splunk has been ramping up its game in this space with 5 acquisitions in this space.

Competitive Advantage

Huge moat with their expandable cloud-native software platform where they could keep adding products/solutions to address adjacent verticals. 2,794 Customers with $111K initial ARR Land for TTM and $251K. Basically, they keep adding six-figure customers suggesting they have a strong GTM and Sales team. They are growing at 30%+ and highly profitable(FCF > 30%).

Key SaaS/Financial Metrics

ARR - $722M

ARR Growth - 35%

Subscription Revenue as part of Total revenues - 93%

Gross Margin - 85%

Free Cash Flow as part of Total revenues - 33%

Net Expansion Rate - 120%+

Rule of 40 - 60%+ (30% growth + 30% FCF)

Debt/Ebitda Ratio - 0.7x

New Customers added TTM - 556(2794 total) = 20%

EV/Revenue TTM - 22x

EV/Revenue NTM(Assuming 30%growth) - 17x

Final Thoughts

Fairly valued, high growth, highly profitable business with a large runaway for further growth.