Pagaya Global - EJFA - AI underwriter and Asset manager

We look at Pagaya Global, a differentiated AI underwriter and Asset Manager with hyper-growth and a long runway for growth

Disclaimer: The information provided is not financial, investment, tax or other advice. Nothing contained constitutes a solicitation, recommendation, endorsement or offer to buy or sell any securities or any other financial instruments. For more information read the disclaimer.

Welcome to the Modern Growth Investing newsletter! If you’re new subscribe below so you don’t miss my weekly updates on growth businesses and investing!

Before you start reading, you might want to click this link to read this article on the website if it doesn’t fit in full in your email.

In this brief I will cover:

What is Pagaya’s Mission?

How do the current Industry Incumbents Lack Innovation and what are their Limitations?

What does Pagaya do?

What are Pagaya’s Products?

How does Pagaya make money?

Who are Pagaya’s Customers?

What is Pagaya’s Market Opportunity?

What is Pagaya’s Growth Strategy to capture this market opportunity?

What is Pagaya’s Competitive Advantage and why is it a durable long-term investment?

What are Pagaya’s People and Culture like?

What do Pagaya’s current Financials look like?

What are my final thoughts on Pagaya AKA TL;DR;?

What is Pagaya’s Mission?

Pagaya has the vision to empower its partners and customers to achieve better outcomes. While the mission is not that inspirational when framed this way, I believe it’s pretty simple and provides lots of opportunities for Pagaya to develop a lot of products.

How do the current Industry Incumbents Lack Innovation and what are their Limitations?

Current lenders use manual, time-consuming processes and bad experiences to lend to consumers. This is undergoing a change by newer lenders like SoFi, Upstart, Affirm, etc to focus on building a great consumer relationship and experience and revolutionize the way consumers get access to credit.

But during this revolution, they have failed to revolutionize their underwriting systems and are still dependent on older systems and data. The banks are using even older systems from decades ago.

Pagaya is taking a stab at improving this by using modern data sources, machine learning, and AI and building a sophisticated AI underwriting system that lenders can plug into using API’s.

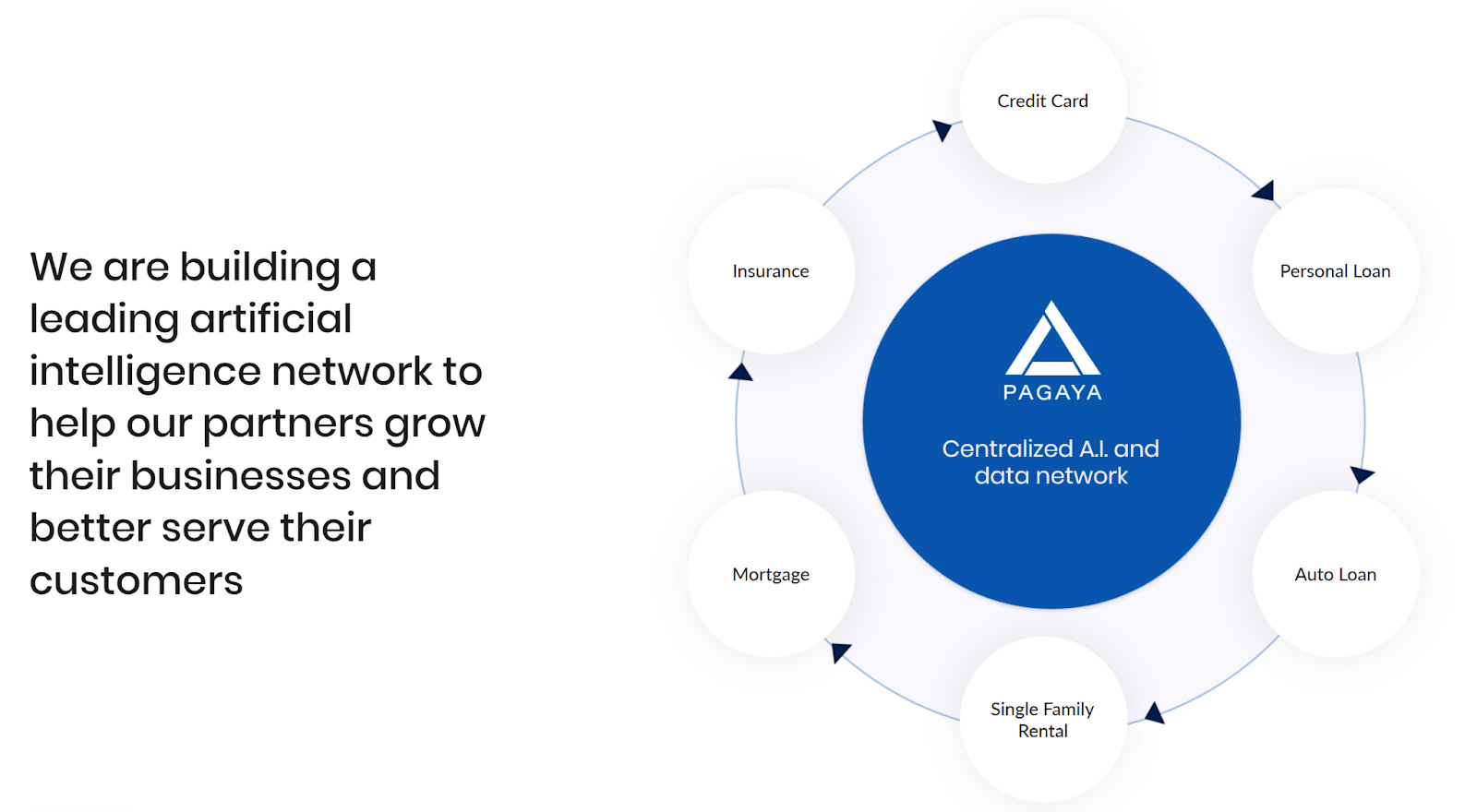

What does Pagaya do?

Pagaya is a centralized AI and data network. They are building a leading artificial intelligence network to help partners to grow their business, and to serve their customers better. The AI network is operated in different markets. In the credit card space, in personal loans, in auto loans, in housing, and in the future, even in insurance and mortgage. This AI is basically the underwriting system that they use to price assets and manage risk.

Pagaya’s ecosystem has 3 players:

Consumer seeking credit

Lending Marketplaces/Lenders

An institution looking to invest in consumer loans

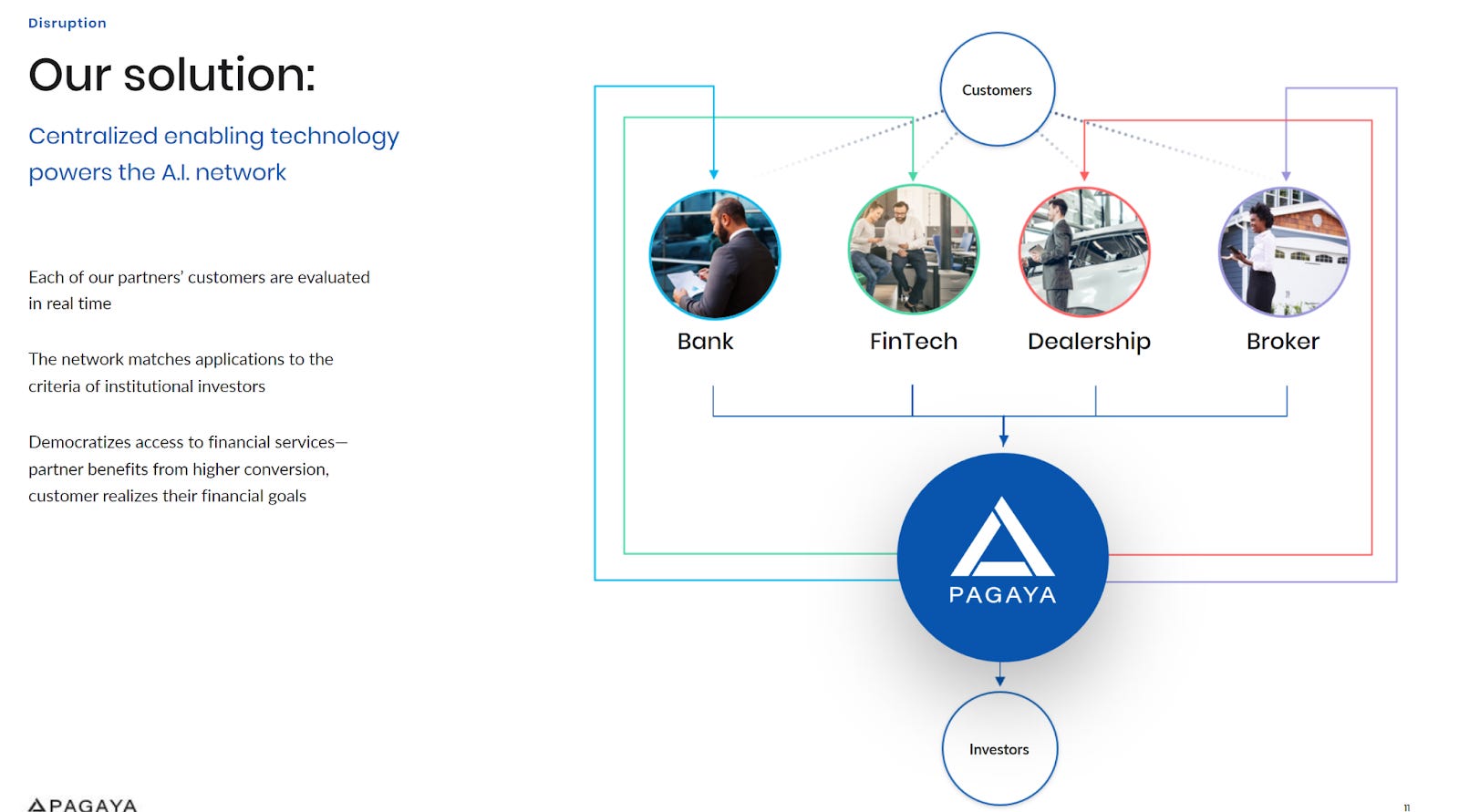

The consumer is going to different lenders, to different service providers, to ask for credit. The lenders are connected to Pagaya with a simple API and when every consumer is coming to consume their credit, pagaya gets their application through that API with all the data of that person. Then they are able to exactly/precisely predict who should get how much credit that person should get and they are more inclusive while doing this using their AI.

Then Pagaya takes this loan and makes it available to an institutional investor who wants to invest in this loan through Asset-Backed Securities.

So Pagaya sits at the center of these 3 parties and gets transaction fees from enabling this seamless end-to-end transaction.

Using Pagaya results in a better outcome for their partners and their customers. Partners are delighted that more customers are being in their ecosystems, and the customers are getting a much better outcome while they are fulfilling their needs or dreams.

In the center of all of that sits the Pagaya AI that is enabling partners to make that outcome through our AI, and to enable the customers to get what they are looking for.

Pagaya provides seamless integration and rapid results. Their partners connect to Pagaya using an API plug-in that enables consumer applications to run through their AI in real-time, and Pagaya is able to approve and transact the applications automatically in real-time.

An interesting thing I noticed is that Pagaya can apply the same process(with different data) for the same consumer for different types of loans eg. personal, point of sale, insurance, mortagage. This gives them tremendous optionality.

As more and more industries are becoming more digital with the availability of more data, Pagaya has the opportunity to expand in more verticals and use its powerful AI to underwrite more verticals accurately. Along with data, the improvements in machine learning, AI, and cloud computing are enabling this transformation.

So over the long term, more and more financial ecosystem participants are going to utilize this efficient underwriting system to lower costs, get better returns and reduce risks. I feel we are very early in this transformation.

At a glance, Pagaya has very vast data, leading technology, with rapid growth and highly scalable. That tech has enabled them to acquire already more than 16 million training data points, which are 100% fully automated, while they are evaluating an application every second, and have managed already to evaluate more than 17 million applications. That has led to very impressive growth. They had almost 200% of a network volume growth annualized in Q2 versus the last year while maintaining 300% of revenue growth in the same period.

The scale is very amazing, with about $4.7 billion annualized network volume in Q2 while creating $381 million annualized revenues.

What are Pagaya’s Products?

Pagaya Started with personal loans and since then has added auto, credit card, Point of sale, and real estate loans, they have also expressed interest in insurance.

How does Pagaya make money?

Pagaya charges transaction fees to their partner’s lenders and institutions to enable the approval of applications and corresponding selling off these loans as securities to the institutional investors.

Who are Pagaya’s Customers?

Some of the marketplace lenders that I could find that are using Pagaya are Upgrade, Marlette, Prosper, Cross River Bank, And LendingClub. And they recently announced A partnership with Sofi. On the institution side, I couldn’t find specific names but they have mentioned institutions, pension funds, and sovereign wealth funds.

What is Pagaya’s Market Opportunity?

The estimated TAM for their products runs into trillions. But I would cap it to $50B and monitor for a long time. I chose $50B as they are currently running $4.7B through their system and I feel a capped 10x TAM is a good measure(realistic) of their TAM for now.

How have they executed to capture this opportunity?

Pagaya has enjoyed about 154% of CAGR just in the last three years. They are now almost $2 billion of origination in the first half of 2021.

Pagaya has been able to grow into new markets at an accelerated pace versus their previous entries in new markets. So, for personal loans, the growth took them 36 months, or 3 years, to reach. In auto, they are seeing much higher growth, and in real estate, even higher. The data and the knowledge from the first market are enabling them to actually penetrate and unlock a different market at a rapid pace.

For Pagaya’s partners, this is an excellent outcome. The AI enables them to very rapidly scale their volume to drive the outcome to the customers. They see 3x median increase in their partners’ volume, only after six months, and 6x of median increase in their partners’ volume when they are on Pagaya 12 months after. This leads to a perfect retention rate(till now).

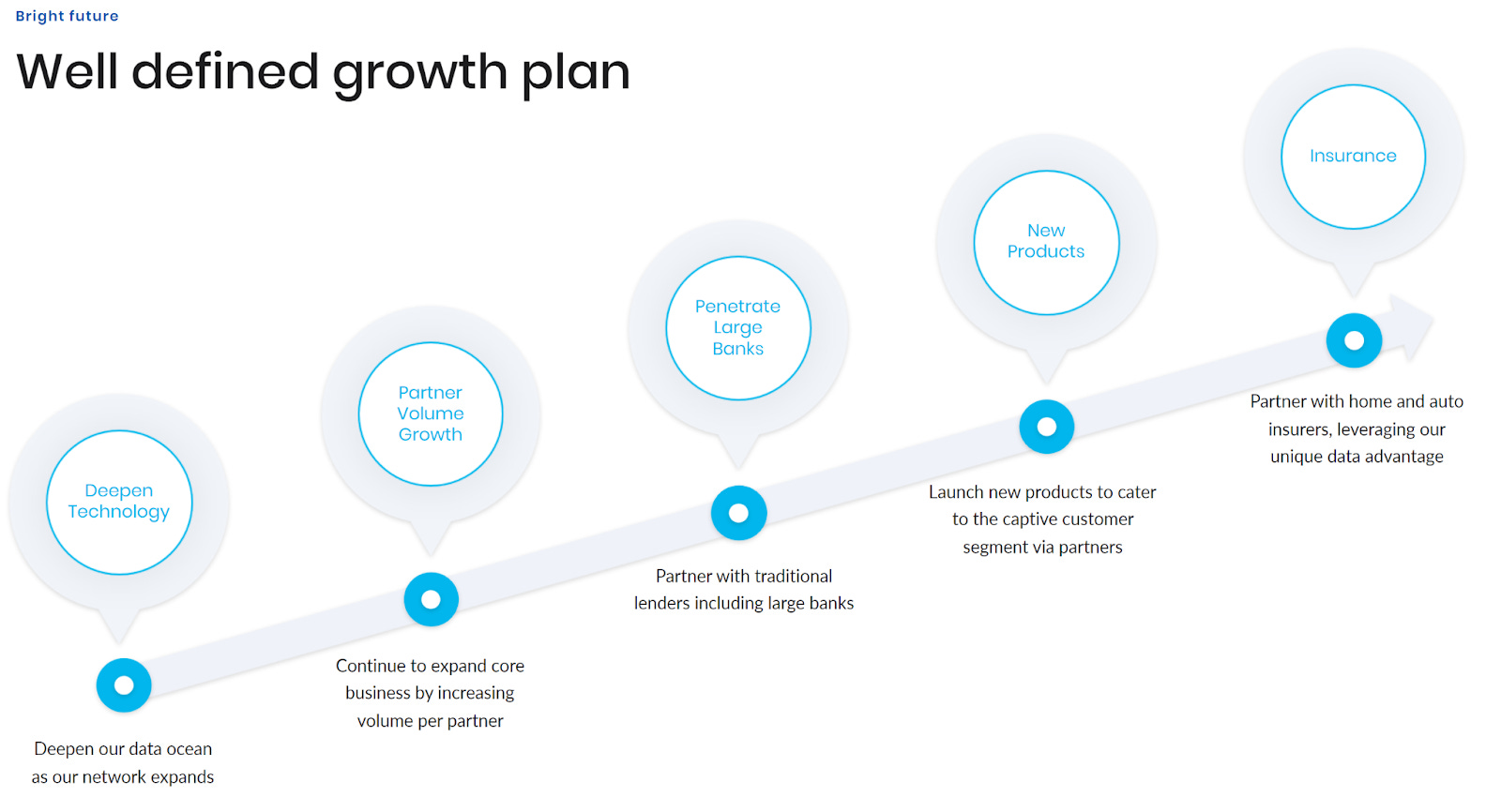

What is Pagaya’s Growth Strategy to capture this market opportunity?

Pagaya’s success will continue to come from multiple growth vectors. As their network grows, their technology gets smarter, and their data becomes more insightful. As their technology gets deeper and richer, their volume and their partners are enjoying that outcome and being able to expand their business. This allows them to enter new markets and to develop new products, leveraging their data advantage to multiply their market share.

The very near-term opportunity is to partner with large banks. The key value proposition is to increase and improve their ability to give the customer’s access to credit, while at the same time, meaningfully increasing their revenue stream.

The banks are keeping the brand loyalty they are looking to have, and keeping the customers in the ecosystem as they found to be able to grow their business, while on the other side, Pagaya is creating a very interesting value proposition to grow their business.

At the same time, the operational efficiency is very high. Because of Pagaya’s easy integration with an API-based infrastructure and real-time processing, there is no real strong overhead associated with that. The potential opportunity is over 60 U.S. banks with $50 billion-plus in assets each, and a combined of $18 trillion as industry assets.

What is Pagaya’s Competitive Advantage and why is it a durable long-term investment?

The deep competitive moat is the data science and the technology that are the foundation of Pagaya(the AI and the Scale). They have a world-class data scientist team and platform of 170 people that are focusing solely on research and development of specialized things which are related to that. They have a tremendous data set, 16 million-plus training data points historically, and a very strong relationship with their partner that brought them to the very unique value proposition that they have today.

Pagaya’s business model is fee-based and capital-light. The fee that they are earning is by selling the assets to the institutional client and earning our AI network fee. All the assets are never originated or serviced by Pagaya, and they’re always Pagaya’s partners servicing end customers. On the other income, they have very limited earns of interest and investment income.

Pagaya has a light balance sheet and low risk funding model while enabling global asset managers, pension funds, sovereign wealth funds, and very strong, well-known institutional clients around the world to participate and to acquire Pagaya’s network into their balance sheet.

Underlying all this I think the core competitive advantage of Pagaya is a network effect of a number of verticals(personal loans, auto loans, etc), marketplace partners(or suppliers), and institutional investors(or demand). A key way to monitor the strength of this effect would be to keep a track of the number of marketplace partners/lenders and investors year over year and also the corresponding volume of the entire network.

What are Pagaya’s People and Culture like?

Pagaya was founded in 2016 by seasoned research, finance, and technology entrepreneurs, and is now 500+ strong in New York, Los Angeles, and Tel Aviv.

Pagaya’s values are:

Continuous Learning: It’s okay to not know something yet, but have the desire to grow and improve.

Win for all: Pagaya exists to make sure all participants in the system win, which in turn helps Pagaya win.

Debate and commit: Share openly, question respectfully, and once a decision is made, commit to it fully.

The Pagaya way: Break systems down to their most foundational element, and rebuild them unique to Pagaya.

What do Pagaya’s current Financials look like?

From the above image, we can see Pagaya has experienced rapid growth recently and they expect this to continue at a slower pace.

They will grow volume to the north of $7.5 billion in 2022 and to nearly $13 billion in 2023. They expect that revenue growth will closely correspond to network volume growth, and they are forecasting to surpass $1 billion of revenue in Fiscal Year 2023.

Over the longer term, given the magnitude of our market opportunity, they should be able to sustain very strong top-line volume and revenue growth for the foreseeable future.

They are investing heavily in research and development and hiring to accelerate their growth. Given the incredible ROI on these investments, they do not expect to prioritize margin expansion in the very near term. That being said, they believe that they can deliver higher margins in the medium term.

We can see a current snapshot of comparison between Pagaya and its peers in the above image. Pagaya seems to be outpacing their peers and is better at execution with product development cadence and scale, all in a relatively short period of time of about 5 years.

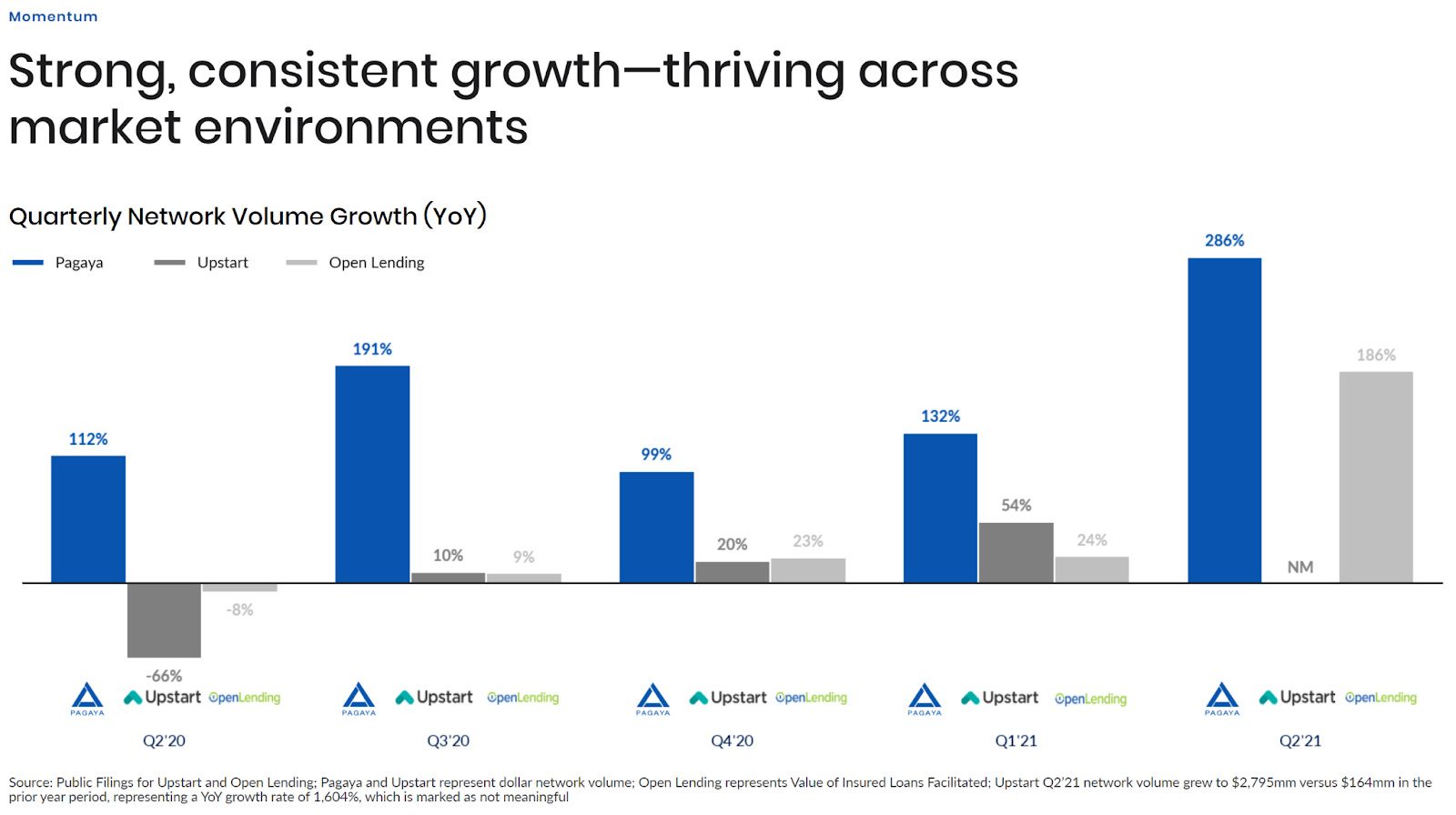

We can see a current snapshot of Quarter over quarter growth comparison between Pagaya and its peers in the above image. Pagaya seems to be outpacing its peers in growth.

The above image gives us an idea about the sponsor. The sponsor is an operator and a leading investor in financial services companies. They have committed $200 million as an investment in the PIPE. Friedman will join Pagaya’s board and he is deeply entrenched in the financial industry. I believe this sponsorship will be an incredible boost for Pagaya.

What are my final thoughts on Pagaya AKA TL;DR;?

Pagaya Global is a highly differentiated AI platform that enables access to credit for consumers, increases outcomes for lenders, and finds really awesome investments for institutions. They have a strong competitive advantage with their network are the intensity of this effect is increasing at a rapid pace. They have rapid product innovation and execution, a founder-led team, and a long runway for high growth. Their heavy investment in R&D coupled with an asset-light approach to underwriting and asset management are their key differentiators.

We are at the end of a brief look at Pagaya. I will do a deep dive on Pagaya when there is more information available about the SPAC merger in their SEC filings for EJFA.

If you love this article and my work, I urge you to subscribe and share.

Thanks, take care.

Modern Growth Investing